News & Updates

Warning: Consolidating or Taking Out a New Federal Loan After July 1, 2026 Could Cost You Your IDR Progress and PSLF Eligibility

Meta description: The July 1, 2026 student loan changes arrived as predicted — but the "consolidation resets your PSLF count" warning was wrong. Here's the real trap.

Federal Watchdog Confirms: Education Department Staff Cuts Are Directly Harming Student Loan Borrowers' Repayment Outcomes

Meta description: Congress warned in 2025 that Education Dept. staff cuts would harm borrowers. The 2026 IG report confirms it—here's what it means and how to protect yourself.

Education Department Quietly Attempts to Revise PSLF Application Form — What Borrowers Must Know Now

PSLF survives July 1, 2026, but SAVE ends and the application form was just revised. Verify your status and pick a qualifying plan now.

Clearing Up Major Misconceptions About the End of SAVE and Your New Repayment Options

Five widely-reported misconceptions about SAVE ending and the new RAP plan, corrected against the regulatory record and what we are seeing on servicer calls. With the operational pathways HC clients should actually consider.

Sweet v. Cardona vs. AFT v. McMahon: Two Lawsuits, Two Different Kinds of Court Oversight — What Borrowers Need to Know

Sweet v. McMahon vs. AFT v. McMahon explained: what each lawsuit promised borrowers, the dated backlog data, and what to do if your forgiveness is stuck.

Student Loan Forgiveness Is Taxable Again in 2026: What Borrowers Need to Know Before the 'Tax Bomb' Hits

IDR student loan forgiveness is taxable again in 2026. Learn how PSLF stays tax-free, how to estimate your bill, and what to do now to plan ahead.

Navient Restitution Checks Are Finally Arriving — Years After Borrowers Were Promised $260 Each

Navient settlement checks promised in 2022 finally arriving in 2026. Learn why the 4-year delay happened and how to claim your payment.

Two New Federal Student Loan Repayment Plans Launch July 1 — Here's How to Choose

July 1 brings new federal student loan plans RAP & Tiered Standard. Compare options, meet deadlines & choose the right repayment strategy.

Parent PLUS Loans and IBR: The New Pathway

How Parent PLUS borrowers can access Income-Based Repayment after consolidation through the ICR grandfathering provision. Includes the two-gate eligibility system, step-by-step pathway, and key deadlines.

The New SAVE Repayment Program: Lower Payments & Student Loan Forgiveness

The New SAVE Repayment Program: What Borrowers Need to Know On August 1, 2023, the U.S. Department of Education launched the SAVE repayment program, replacing the REPAYE program. This new plan is designed to provide more generous benefits for student loan borrowers. Below are the key aspects of this

Student Loan Forgiveness 2024: New Programs and Expanded Benefits

Student Loan Forgiveness 2024. In the past few months leading up to the return to repayment, student loan borrowers have seen significant new benefits aimed at reducing repayment costs and increasing student loan forgiveness. Now, the U.S. Department of Education is pushing for even more targeted fo

DEADLINE: WHAT BENEFITS ARE EXPIRING ON 12/31/2023?

## Student Loan Forgiveness: Urgent Deadline for FFEL and Parent Plus Loan Borrowers April 30, 2024: Key Deadline for Student Loan Consolidation April 30, 2024, is the new deadline to consolidate FFEL or Parent Plus loans into a Direct Consolidation Loan to remain eligible for the IDR One-Time Accou

Federal Register Updates - Student Loan Regulatory Changes

Track the latest Federal Register updates affecting student loan borrowers, including regulatory changes, comment periods, and implementation timelines.

Important Dates - Student Loan Deadlines & Milestones

Key dates and deadlines for student loan borrowers including repayment milestones, program deadlines, and regulatory timelines.

Student Loan Servicer Performance Analysis

Comprehensive analysis of student loan servicer performance data, error rates, and accountability metrics from 2015-2024.

Student Loan Delinquency Rates - Statistical Analysis

In-depth statistical analysis of student loan delinquency rates, trends, and their impact on borrowers across different demographics.

SAVE Plan Legal Impact Analysis

Analysis of ongoing legal challenges to the SAVE plan, court rulings, and the impact on student loan borrowers and repayment options.

Foreign Student Loans - International Student Loan Statistics

Statistical overview of international student loan debt, trends in foreign student borrowing, and the impact on the broader student loan landscape.

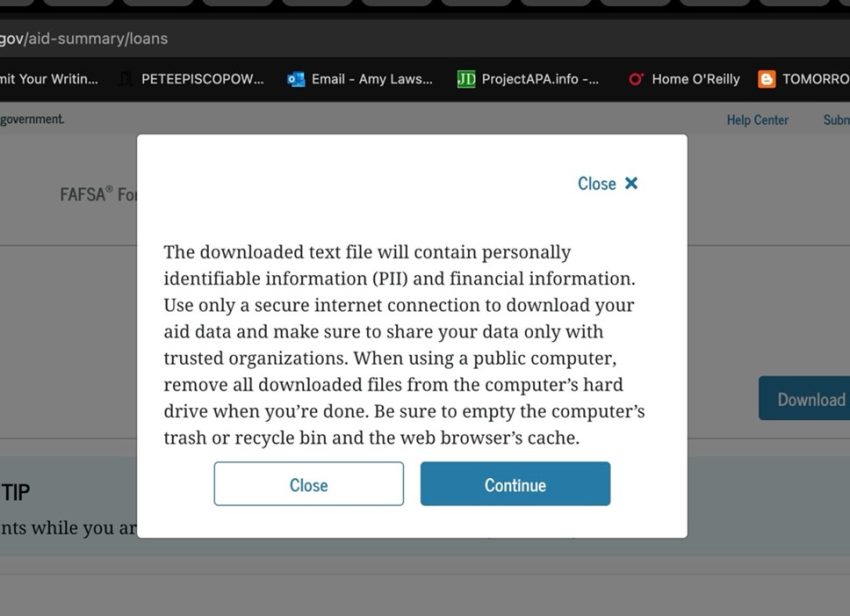

How To Access and Download Your Federal Student Loan Data File

Step-by-step instructions to download your federal student loan data file (MSD) from StudentAid.gov on Mac, PC, iPhone, and Android devices.

PSLF Waiver - Limited Time Student Loan Debt Waiver

According to the U.S. Department of Education, the PSLF Waiver program could benefit more than half a million student loan borrowers once they consolidate into the Direct Loan Program.